Imagine working tirelessly, literally all year, just to grow your business. You know, pouring every single ounce of your energy into your team, into your clients, into the specific services you provide. And then you discover at the end of the year that you have unknowingly tipped the government tens of thousands of dollars. Not because you did anything wrong. I mean, not because you broke a rule, but simply by default.

It really is a startling scenario when you put it like that. You know, you look at the final numbers, the dust settles on another tax season, and you realize that your biggest, most uncontrollable expense for the entire year was… well, it was actually entirely avoidable.

Yeah, and that scenario is exactly what we are tackling in today’s deep dive. We are looking at this fascinating stack of documents detailing the proactive methodologies of a firm down in Texas called O&M Tax and Business Advisory.

Yeah, it’s a great case study. It really is. So our mission today is to uncover exactly how service-based business owners, specifically those operating in the Rio Grande Valley, are utilizing this firm’s framework. We want to see how they’re flipping tax season from a stressful last-minute scramble into a year-round profit center.

And to really grasp how they’re pulling this off, we have to start by fundamentally redefining who is actually handling your money. Because when most people hear the word taxes, they immediately picture, you know, a reactive tax preparer.

Right. Like the person you see once a year in April.

Exactly. You know the routine. You hand them a chaotic spreadsheet or like literally a shoe box of receipts in early April and they just punch those historical numbers into a computer system. But O&M operates under a completely different paradigm because they are an Enrolled Agent firm.

Okay, let’s unpack this. Because that distinction between a seasonal reactive preparer and a credentialed proactive Enrolled Agent seems to be the exact fault line where all this money is falling through. So what is an enrolled agent exactly?

Right, so an Enrolled Agent or EA holds the highest tax credential awarded directly by the IRS. They are federally licensed. So they don’t just act as data entry clerks. They have the absolute authority to represent clients before the IRS in audits, appeals, collections, all of it.

Wait, directly by the IRS? This isn’t just a weekend certification course.

Oh no, not at all. It is a completely different tier of legal and strategic expertise. It takes rigorous testing and background checks.

Okay, so I want to understand the mechanics here. Why does having an EA building a proactive strategy actually change the math for a business owner’s bottom line? Like, where is the money actually leaking out?

It comes down to understanding the anatomy of an overpayment. The documents we are analyzing outline five very distinct leaks that occur when you rely on a reactive system. These are the traps that just bleed money from business accounts every single year.

Okay, what’s the first trap?

The very first trap is the simple act of waiting. If you have absolutely no year-round planning, you know, if you just wait until April, you have already lost.

Right. So just the timeline itself is a penalty.

Yes, essentially. Because if your tax professional only hears from you in March, the calendar year is closed. You can’t retroactively go back to November and change how you spent your capital.

That makes sense. Relying on a tax preparer in April is like, I don’t know, going to a doctor after you’ve already broken your leg and expecting them to teach you how to prevent the fall. It’s just too late.

That is exactly it. By spring, you aren’t strategizing. You are just reporting history to the government. If you want to utilize the tax code to your advantage, that maneuvering has to happen in January, in June, in October.

Right. And that lack of early planning leads directly into the second and arguably most devastating pitfall, which is operating under the wrong business structure.

Yeah. This one is a massive leak for high-earning service providers.

Yeah. This specific point in the research completely blew my mind. We are talking about businesses that are operating as sole proprietors or single-member LLCs when they actually should be structured as S-corps.

But how does that actually work? Why does a different acronym at the end of your company name change your tax bill so drastically?

Well, it has to do with how the IRS classifies your income. When you operate as a standard LLC or a sole proprietor, the IRS views all of your business profit as self-employment income.

Okay. Let’s use some real math here. Say your business nets $200,000 in profit. Under an LLC, you are hit with a 15.3% self-employment tax on that entire amount.

And that covers like Medicare and Social Security, right?

Right. Exactly. And that hits you before you even touch your regular income taxes. So 15.3% of 200,000, that’s over $30,000 gone instantly.

Just a self-employment tax alone, that’s brutal.

Correct. But if an advisor restructures you as an S-corporation, the mechanics change entirely. An S-corp allows you to split that income. You are required to pay yourself what the IRS calls a reasonable salary through payroll.

Okay. So let’s say I pay myself a salary of $80,000.

Perfect. So you only pay that 15.3% self-employment tax on the $80,000 salary. The remaining $120,000 of profit is taken as an owner’s distribution.

Which completely bypasses that self-employment tax.

Yes, exactly. It completely bypasses it.

Let me make sure I have this straight because this is huge. By simply utilizing an S-corp structure, you shelter that $120,000 from the 15% tax hit. So you just saved what? Over $18,000 in cash?

Yes. Just from having the correct legal structure in place.

Wow. And the tragedy is that most owners have absolutely no idea this mechanism exists until someone like a proactive EA points it out. Which brings us to the third leak: missed deductions and credits.

Right, because everyone hears about home office deductions or vehicle expenses or, you know, retirement contributions. But there’s more to it than that, isn’t there?

Much more. There are complex mechanisms like the Qualified Business Income deduction, or QBI.

Yeah, I saw QBI mentioned in the sources. What exactly is that? It sounded pretty complicated.

It is a bit complex, yeah. QBI is a relatively recent tax provision that allows certain pass-through business owners to deduct up to 20% of their qualified business income right off the top.

20%. That is a massive tax shield.

It really is. But here is the catch. It is highly complex. If your income crosses a certain threshold, the deduction starts to phase out. To keep it, you have to execute specific maneuvers. Like paying out a certain amount of W-2 wages or investing in qualified property.

Which goes right back to your first point about timing.

Mm-hmm. A reactive tax preparer in April can’t help you with QBI. If you made too much money, they just tell you the bad news. They don’t have a time machine to go back and tell you to run more payroll in December to save your 20% deduction.

Exactly. You are treating the symptom of a high tax bill, but you are doing absolutely nothing to prevent the injury from happening in the first place. That brings up a great analogy from the notes. Operating this way is like driving down a highway at night with your headlights completely off, trying to steer the car by only looking in the rear-view mirror of last year’s tax return.

Right. You are definitely going to crash.

That perfectly illustrates the fourth leak: having no cash flow visibility. Without clean, reliable monthly bookkeeping acting as your dashboard, you are flying blind. You are making major business decisions… like whether to hire new staff or buy expensive equipment or sign an expansion lease, without the actual financial data to tell you if you can afford it. Or how those decisions will impact your end-of-year tax liability.

Exactly. Which naturally feeds into the fifth and final trap in this reactive cycle, which is growing overhead with absolutely no control.

Right. The cost of software subscriptions, insurance, raw materials, it all just keeps rising.

Yeah. And without a financial system acting as a guardrail, you end up making incredible gross revenue. But your margins shrink so much that you feel like you’re constantly scrambling just to cover payroll.

It’s crazy. See, what’s fascinating here is how interconnected all these problems are. Like, the structure dictates the taxes, the timing dictates the deductions, and the bookkeeping dictates the visibility. Once you see the anatomy of this trap, the immediate question is how a firm like O&M actually intervenes to stop the bleeding.

Right. So let’s transition into their actual framework. The sources outlined a deeply integrated system. It’s not just a menu of random accounting services. So where does an Enrolled Agent firm even begin when a new client walks in the door with a messy financial history? Do they just jump straight into the taxes?

No. They attack the foundation first through comprehensive business formation and restructuring. If you are starting a business or if you’ve been running one and suspect your structure is bleeding money like our S-Corp example earlier…

Yeah.

They analyze your income trajectory, your industry risks, and your long-term goals.

Okay.

Then they implement the precise entity you need. And they handle the heavy lifting. The EIN registration, drafting the operating agreements, and filing the exact tax elections with the IRS.

So what does this all mean? Let me push back on this a bit because I hear this exact logic all the time from new entrepreneurs. If I can go onto a legal website and file an LLC myself for like 100 bucks, why do I need a whole advisory service to do it for me? Isn’t an LLC just a standard form?

It is a completely fair question. And the sources actually provide a brilliant counter-example with a client named Op Vargas.

Oh right, the DIY story.

Yeah. Op assumed the DIY route was sufficient. But when you use a basic online filing service, you are essentially just buying a name tag for your business. You aren’t building a real legal shield. Op missed vital foundational steps.

Like what?

Well, he didn’t secure an EIN properly. He had no formal operating agreement, and he missed the strategic tax elections entirely.

Wait, how dangerous is it to skip something like an operating agreement? I mean, doesn’t the LLC status just protect you automatically?

It could actually be catastrophic. If you are ever sued, and the court sees that you don’t have an operating agreement or proper corporate formalities in place, they can execute something called piercing the corporate veil.

Piercing the corporate veil. That sounds intense.

It is. The judge basically declares that your LLC isn’t a real company at all. It’s just an alter ego for you personally. And suddenly the liability shield vanishes, and your personal assets—you know, your home, your personal savings—they are entirely exposed to the lawsuit.

Oh wow. So O&M had to step in and rebuild Ope’s entire structure from the ground up to actually protect him.

Right.

Okay, so buying the cheap online LLC is basically like buying a bank vault but forgetting to install the lock. The appearance of security is there, but the mechanism is just totally missing.

That’s a great way to put it. So once they fix that structural bleeding, how do they ensure the business doesn’t just fall back into bad habits? Because it’s easy to get lazy again.

That is where their signature methodology comes into play. Strategic tax planning. This is the antidote to that rear-view mirror approach we talked about.

Okay, so what does that look like in practice?

It is a written, customized tax strategy built specifically for your business. And it’s delivered well before tax season even begins. They prioritize quarterly optimization. A huge part of this is timing your business purchases correctly to maximize deductions.

Let’s talk about the mechanics of that timing. Give me an example of how buying something in December versus January changes everything.

Let’s look at heavy equipment or vehicles. The tax code has a provision called Section 179, which allows businesses to deduct the full purchase price of qualifying equipment in the year it was placed in service, rather than depreciating it slowly over five or ten years.

Right, so you get the whole tax break up front.

Exactly. So if your Enrolled Agent sees in November that you are on track for a massive tax bill, they might advise you to purchase that $50,000 work truck you’ve been needing before December 31st.

Okay.

By utilizing Section 179, you instantly knock $50,000 off your taxable income for that current year.

And if you wait…

If you wait until January 1st, that deduction gets pushed to the following year, and you are stuck paying taxes on that 50 grand right now.

That is a phenomenal example. It’s active maneuvering. But I mean, to know you have that 50 grand available in November, your day-to-day numbers have to be flawless. Which brings us to how they handle bookkeeping, right? Because they don’t seem to treat it as a compliance chore just to keep the IRS happy.

Not at all. They utilize bookkeeping as a real-time business intelligence tool. It is the dashboard with the headlights turned on.

Nice callback.

Thanks. The goal is to keep your financials meticulously organized every single month, so you always know your exact profit margins and your cash position.

So it completely eliminates that desperate scramble to reconstruct 12 months of receipts in March.

Exactly. But more importantly, it allows the tax strategy to pivot if your business suddenly, say, doubles its revenue in the middle of summer.

Yeah, you can actually adapt. And when you have the structure, the year-round strategy, and the real-time bookkeeping all talking to each other, the final step—actual income tax preparation—well, it becomes a total non-event.

It becomes a victory lap, essentially. By the time filing season arrives, the heavy lifting is completely done. Both the business and personal returns are smooth and accurate because every single strategy built throughout the year is seamlessly and legally reflected on that final return.

Okay, so the theory is incredibly sound. The mechanics make perfect logical sense. But for you, the listener, theory is only as good as the reality it produces. So does this actually work? Let’s talk about the real numbers, because the data we pulled from these sources is honestly jaw-dropping.

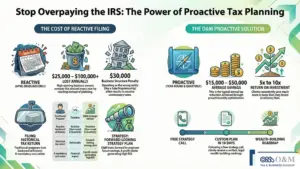

It is. When we look at the return on investment for this comprehensive approach, O&M clients are saving an average of $15,000 to $50,000 per year in taxes.

Every single year.

Every single year. And to put that into perspective, clients consistently save 5 to 10 times more in taxes than they actually invest in O&M’s advisory services. In some exceptional cases, they are uncovering $25,000 to $100,000 in legal tax savings.

Okay, let me challenge those numbers for a second. We’re throwing around figures like $50 to $100,000 in tax savings. Are we talking about multinational mega-corporations here? Because that level of cash seems entirely out of reach for a regular local service business.

I get why you’d think that. It is a really common misconception, but no. The data shows that the average successful service-based business owner—say a local roofing company, a medical clinic, or a consulting firm netting a few hundred thousand dollars a year—is often paying well over $50,000 annually in taxes simply due to poor structuring.

So these aren’t Fortune 500 secrets.

Not at all. These massive savings aren’t for Wall Street. They are specifically for local business owners who just haven’t been taught how to optimize their financial architecture.

That is wild. You just don’t realize how much you are bleeding until someone shows you the math. And this brings up a crucial dynamic from the sources regarding O&M’s specific location. They are deeply embedded in the Rio Grande Valley, serving Edinburg, McAllen, Mission, Pharr, Weslaco, Brownsville… that entire South Texas metro area.

If we connect this to the bigger picture, you start to see why local, culturally fluent financial advice is a superpower. The Rio Grande Valley has a unique economic landscape. O&M isn’t some faceless national chain that parachutes into town in February. They offer full, high-level professional support in both English and Spanish.

I would imagine the bilingual aspect is absolutely critical. I mean, we just spent 10 minutes breaking down the complexities of S-Corp, QBI, and Section 179 depreciation. Trying to navigate those incredibly dense financial concepts is hard enough in your native tongue.

Exactly. If English isn’t your primary language, losing the nuance of a sophisticated tax strategy in translation could literally cost you your business.

Absolutely.

Having an Enrolled Agent who understands the local industries and can communicate these complex strategies clearly in your preferred language builds an incredible foundation of trust. And the client reviews from the Valley really back up this methodology.

Yeah, I saw a few in the notes. There was one from Rocky Garza, right?

Yes. Rocky worked with an advisor at O&M named JC. Rocky specifically praised the proactive communication, noting that JC saved him both time and money by actively hunting down deductions rather than just waiting to be told what to do.

And we see that sentiment repeated across different industries, too. Rachel Gambetta noted that O&M helped restructure her business for long-term savings, praising their proactive nature by saying they are, quote, “always a step ahead.” And then Jose Juan Garcia summed it up as an A-to-Z, excellent service, highlighting the dedicated professionalism of the management team. It’s really the whole package.

It really is. So, having proven the mechanics of the strategy and the reality of the results, the logical next step is understanding the blueprint itself. If you are a business owner listening to this, analyzing your own financial leaks, you are probably wondering how a firm like this actually onboards a new client to stop the bleeding.

Right. How do you practically transition into this model?

Well, the sources outline a highly transparent three-step onboarding process. Step one is a free strategy call.

Okay. What happens on that call?

They sit down with you. Review your current income. Look at how your business is legally structured, and analyze your past tax approach. There’s no cost to just look under the hood.

That’s great. No risk there.

Step two is the actual deliverable. Within just 10 days of that initial consultation, they provide a written plan. It is a custom document outlining your exact savings potential and the specific legal steps required to restructure your finances.

So it’s a concrete roadmap, not just a vague promise.

Exactly. And step three is ongoing support. You get those quarterly meetings and actual help with implementation as your business grows and as tax laws inevitably change over time.

But we should be very clear about who this is actually for, right? Because O&M is highly specific about their target audience.

They are. This level of intensive advisory is specifically designed for business owners earning over $300,000 in revenue who want legal, defensible, year-round strategies.

Here’s where it gets really interesting. What if a listener is hearing all this, realizing their books are a total disaster… They are way behind on their taxes, and they just want a quick, cheap filing to get the IRS off their back. Can they just call O&M for a quick fix to catch up?

The short answer is no. And O&M is radically transparent about this up front. If you are looking for aggressive shortcuts, questionable deductions, or just a one-time band-aid reactive filing, they will tell you immediately that is not what they do.

So they don’t do the quick fixes.

No. Their entire firm is built on defensible, legal strategy that can withstand an IRS audit. They protect their clients by refusing to cut corners.

I love that level of clarity. You know exactly what you are getting. If you are a business owner in the Valley who fits that profile—earning over 300k, ready to stop reacting and start proactively strategizing—you need to know how to connect with them. Their physical office is located at 4414 South Raul Longoria Road, Suite B in Edinburg. You can call them directly at 956-855-3880. And of course, everything we discussed today is available online at onmservices.com. Plus, they maintain a strong presence across social media, including Facebook, Instagram, LinkedIn, and TikTok.

When you look at the totality of these sources, a very undeniable thesis emerges about how we view money. Strategic tax planning is not an expense. When a specialized advisory firm consistently saves you 5 to 10 times what you pay them in fees, that is an investment. It is a fundamental shift in how you allocate and protect your capital.

It pays for itself over and over again.

And that is the biggest takeaway for you, the listener. If you are a high-earning business owner and you haven’t had a proactive, strategic conversation about S-Corp, QBI, or depreciation this year, you are quite literally leaving your own hard-earned money on the table for the government to sweep up.

This raises an important question. I’m listening.

We have a tendency to view the tax code as this oppressive, fixed list of rules and penalties that we just have to suffer through.

Yeah.

But what if we shifted our perspective entirely?

Oh, yeah.

The tax code is actually a massive map of government incentives. It is the government telling you exactly how they want you to structure your business, how they want you to hire employees, and when they want you to invest your money into the economy.

Wow. Yeah.

If you aren’t proactively planning your taxes, are you simply penalizing yourself for refusing to learn the rules of a game you are already forced to play? Think back to that opening thought. Unknowingly tipping the government tens of thousands of dollars simply by default. What could you do with an extra $50,000 in your business this year… if you finally decided to learn the rules.